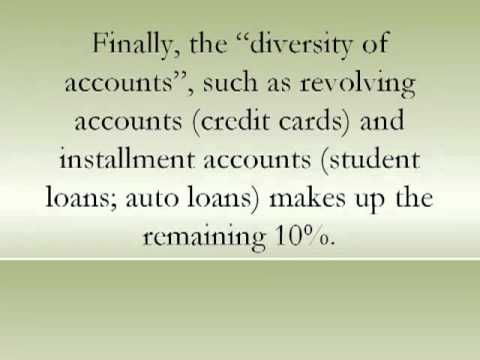

For many years, FAIR ISAAC, the creator of the FICO credit score kept consumers in the dark about the existence of their credit scores. Even today, knowing how credit scoring works is a secretive science for most folks. A reason why 61 million Americans have subprime credit scores (ranging from 500 to 649) is that credit bureaus are in the business of selling “negative’ data. Thus, the more illiterate people are about credit bureau practices, the less creditworthy they are to potential lenders. HOWEVER… …The following 7 misconceptions and facts will give you a broader perspective about managing your credit standing: Misconception #1: “Personal information cannot be deleted from a credit report.” Fact: Even if it’s a bankruptcy, any credit information that is not 100% complete, exact, or verifiable can be erased from your credit profile. This has been the case since passage of the Fair Credit Reporting Act, a federal law decreed by Congress in October 26, 1970 that allows you to dispute any inaccurate information on your credit report with the party that reported it. When you file a dispute, the furnisher must re-investigate the dispute and if the information is found to be inaccurate, incomplete, or can no longer be verified, they must permanently delete it from your credit file. Misconception #2: “Payment history makes up your consumer credit score.” Fact: Many people believe that the “payment history” is what makes up their credit scores. But, your bill paying habit only makes up 35% the scoring. A second category, the “debt-to-credit t ratio” (the ratio of the account balance to its credit limit), makes up another 30%. A third category, “length of credit history” (the age of your accounts), makes up 15%. A fourth category, “number of hard inquiries” (new credit applications), makes up 10%. Finally, the “diversity of accounts”, such as revolving accounts (credit cards) and installment accounts (student loans; auto loans) makes up the remaining 10%. Thus, all five categories weigh in on your final numeration. Misconception #3: “You have only one consumer credit score.” Fact: Each credit bureau assigns you a different credit score, each ranging from 300 to 850 points. Equifax uses the BEACON score, Trans Union uses the EMPIRICA score, and Experian uses the FICO score. Misconception #4: “Paying off collection accounts improves your credit.” Fact: Paying off a collection account can actually hurt your credit. This automatically resets the account’s required seven year reporting period from the date of last activity or when the account was paid. Essentially, if the collection account only has one more year to remain on your report, as soon as pay it off, it renews the reporting period giving you 7 more years of bad credit. Misconception #5: “Closing inactive accounts and opening new accounts improves your credit score.” Fact: The length of your credit history contributes to 15% of your score. Thus, the older your accounts, the higher your points. And your account must be open a minimum of 12-months in order to be scored. So, rather than opening a new account, you should “activate” inactive accounts and begin making credit purchases on them. This activity will also improve your payment history, a category that makes up roughly one third of your credit score. Misconception #6: “All credit inquiries hurt your credit score.” Fact:There are two types of credit inquiries, “soft inquiries” and “hard inquiries.” Soft inquiries are inquiries made by creditors, landlords, or employers. These inquiries do not affect you. However, when you submit an application for credit and the creditor requests a copy of your report, you are making a “hard inquiry, which will affect your scoring. Making too many hard inquiries within a proximate timeframe can hurt your future opportunities to obtain loans. Misconception #7: “A bankruptcy filing must appear on your credit report.” Fact: Contrary to popular belief, federal and states courts are not required to report any type of public record. A bankruptcy would only appear on your consumer credit report because the credit bureau sent an employee or independent contractor to the courthouse to gather the public record. The good thing is that credit bureaus generally report inaccurate information that you can delete through the dispute process. In conclusion, separating the facts from the myths about credit scoring and your credit report gives you essential ingredients to boost scoring. Vic Chevalier is a financial coach and author. He has written many articles for http://www.DebtFreeLeague.com and numerous blogs with the aim to empower people to achieve financial prosperity. Many of his topics offer invaluable debt relief and credit restoration tips. Article Source: http://EzineArticles.com/?expert=Vic_Chevalier

|

|

||

|

|

|||

Archive for the ‘Credit Repair’ Category.

Generally, people who are in debt shun credit card settlement as a debt relief solution, seeing it as antithesis to good credit. However, this is a serious myth. Although the procedure can lead to bad credit, you’re about to see it is also one of the best credit solutions. The following credit scenarios illustrate how credit card settlement can be the right prescription to repair bad credit: Paying on time, but maxed out on credit cards… If you tapped into most or all of your available lines of credit, your credit took a serious hit. Maxing out your credit limits creates the undesirable effect of a high debt-to-credit ratio, which kills good credit. The debt-to-credit ratio compares how much credit is available to your credit line. Credit card issuers use this formula to determine if it’s safe to grant you additional lines of credit. The debt-to-credit ratio is significant since it makes up one third of your FICO credit score. An optimum debt-to-credit ratio is 30% or below, meaning that you used 30% or less of your available credit. At a 40%, it tells banks that a financial hardship is brewing. But, the real credit threat is having a debt-to-credit ratio of 50% or greater, which is the case of most debtors. Paying on time, but living paycheck-to-paycheck Even if you pay on time, if you have a lot of debt and are squeezing to make the minimum payment, you have the misfortune of a high debt-to-income ratio. Thus, you’re perpetuating bad credit. Major credit issuers, like mortgage companies, rely heavily on the debt-to-income ratio to grant consumer credit. The formula compares your monthly income against the combined monthly payments on your credit cards, bank loans, car and mortgage loans, and student loans and/or tuition. Like the debt-to-credit ratio, having a debt-to-income ratio of 50% or greater means that “you owe more than what you can reasonably pay.” The way lenders see it, if you can’t show disposable income, why give you more credit? Being in this position, it shouldn’t surprise you if you got turned down for mortgage loans, your credit limit got lowered, or if you’re only receiving credit offers for high interest credit cards. Not making the minimum payment Obviously, if you don’t make the minimum payment on time, your credit score will decline. Likewise, credit card settlement is a procedure that can cause your credit score to go down. This happens because people that resort to this practice quit struggling to throw away money on endless minimum payments. Instead, they try a faster way to get out of debt and save hard-earned money to settle credit card balances. Consequently, if you default on any terms of your credit card agreement, expect “late payments”, “collection accounts”, and other derogatory credit items on your credit report. FACT: “Credit card settlement can fix bad credit” If you meet any of the above credit scenarios, credit card settlement is an excellent option amid the mix of credit solutions. First of all, the effect on your credit score may be negligible to the damage you may have already caused on your credit report. Secondly, it helps you successfully get rid of debt at a much faster pace than the minimum payment approach. Credit card settlement is a more aggressive debt elimination approach compared to the doldrums of the minimum payment. It produces an agreement between you and the credit card company to pay off your credit card balance subject to a massive reduction on principal, interest, and fees. What better way to pay off your credit cards for pennies on the dollar and become debt-free? In conclusion, in weighing the debt elimination and credit solutions, credit card settlement is a top contender. Not too many credit solutions offer such a fast transition from the rut of living paycheck to paycheck and bad credit to the enjoyment of financial stability and better credit.

|

|

||

|

|

|||