|

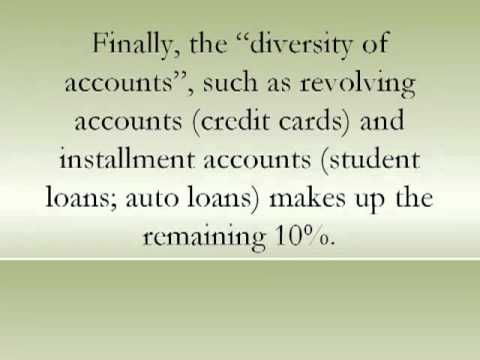

For many years, FAIR ISAAC, the creator of the FICO credit score kept consumers in the dark about the existence of their credit scores. Even today, knowing how credit scoring works is a secretive science for most folks. A reason why 61 million Americans have subprime credit scores (ranging from 500 to 649) is that credit bureaus are in the business of selling “negative’ data. Thus, the more illiterate people are about credit bureau practices, the less creditworthy they are to potential lenders. HOWEVER… …The following 7 misconceptions and facts will give you a broader perspective about managing your credit standing: Misconception #1: “Personal information cannot be deleted from a credit report.” Fact: Even if it’s a bankruptcy, any credit information that is not 100% complete, exact, or verifiable can be erased from your credit profile. This has been the case since passage of the Fair Credit Reporting Act, a federal law decreed by Congress in October 26, 1970 that allows you to dispute any inaccurate information on your credit report with the party that reported it. When you file a dispute, the furnisher must re-investigate the dispute and if the information is found to be inaccurate, incomplete, or can no longer be verified, they must permanently delete it from your credit file. Misconception #2: “Payment history makes up your consumer credit score.” Fact: Many people believe that the “payment history” is what makes up their credit scores. But, your bill paying habit only makes up 35% the scoring. A second category, the “debt-to-credit t ratio” (the ratio of the account balance to its credit limit), makes up another 30%. A third category, “length of credit history” (the age of your accounts), makes up 15%. A fourth category, “number of hard inquiries” (new credit applications), makes up 10%. Finally, the “diversity of accounts”, such as revolving accounts (credit cards) and installment accounts (student loans; auto loans) makes up the remaining 10%. Thus, all five categories weigh in on your final numeration. Misconception #3: “You have only one consumer credit score.” Fact: Each credit bureau assigns you a different credit score, each ranging from 300 to 850 points. Equifax uses the BEACON score, Trans Union uses the EMPIRICA score, and Experian uses the FICO score. Misconception #4: “Paying off collection accounts improves your credit.” Fact: Paying off a collection account can actually hurt your credit. This automatically resets the account’s required seven year reporting period from the date of last activity or when the account was paid. Essentially, if the collection account only has one more year to remain on your report, as soon as pay it off, it renews the reporting period giving you 7 more years of bad credit. Misconception #5: “Closing inactive accounts and opening new accounts improves your credit score.” Fact: The length of your credit history contributes to 15% of your score. Thus, the older your accounts, the higher your points. And your account must be open a minimum of 12-months in order to be scored. So, rather than opening a new account, you should “activate” inactive accounts and begin making credit purchases on them. This activity will also improve your payment history, a category that makes up roughly one third of your credit score. Misconception #6: “All credit inquiries hurt your credit score.” Fact:There are two types of credit inquiries, “soft inquiries” and “hard inquiries.” Soft inquiries are inquiries made by creditors, landlords, or employers. These inquiries do not affect you. However, when you submit an application for credit and the creditor requests a copy of your report, you are making a “hard inquiry, which will affect your scoring. Making too many hard inquiries within a proximate timeframe can hurt your future opportunities to obtain loans. Misconception #7: “A bankruptcy filing must appear on your credit report.” Fact: Contrary to popular belief, federal and states courts are not required to report any type of public record. A bankruptcy would only appear on your consumer credit report because the credit bureau sent an employee or independent contractor to the courthouse to gather the public record. The good thing is that credit bureaus generally report inaccurate information that you can delete through the dispute process. In conclusion, separating the facts from the myths about credit scoring and your credit report gives you essential ingredients to boost scoring. Vic Chevalier is a financial coach and author. He has written many articles for http://www.DebtFreeLeague.com and numerous blogs with the aim to empower people to achieve financial prosperity. Many of his topics offer invaluable debt relief and credit restoration tips. Article Source: http://EzineArticles.com/?expert=Vic_Chevalier

|

|

||

|

|

|||

This article has truly been enlightening. I tend to have the belief that human beings have made things (like credit scoring) unnecessarily complicated. The fact that most people (the “hoi polloi”) do not understand credit scores is part ignorance, and part sheer complexity of the system that has been created. It should also be pointed out that many people, including myself, maintain ignorance about our credit scores simply because they do not effect us on a day to day basis. I’ve been trying to get out of this rut, though, and learn at least some basics about them as I am preparing to make some large purchases (a house specifically) within the next few years; so I would imagine having a nice credit score would make securing a home much easier on my part.

Anyways, getting off of “myself” here; I’d say these are some solid misconceptions about credit scores. Though, I would have to admit that some of them seem rather unfair like the effects of closing an account and reopening another one. That just seems like a rather arbitrary reason to judge someones ability to successfully pay back credit debts, but I’m going to guess there is good reason for it. I look forward to seeing what you more you have to say with regards to credit on this blog! Thanks for the information!

I have heard numerous claims about credit repair and the truth is I was somewhat of a skeptic. I thought it was some kind of scam. But, thanks to informative articles like the one at DebtFreeLeague Blog, I’m gradually finding that most of the information out there attacking credit repair is pure propaganda. It seems the system wants you to think there’s nothing you can do to fix your credit. I read somewhere that erroneous data appears in about 80% of all credit reports. But I also read the Fair Credit Reporting Act lets you challenge a lot of the false junk the credit bureaus report. Just because you owe a debt doesn’t mean it is being factually reported and if it’s not 100% accurate, they are violating the law. Equifax reports that I owe about $3,000 on an old Verizon account. Many years ago I challenged this debt with Verizon, which was only several hundred at the time. I’m wondering if you can give me any tip to get this inaccurate item off my credit report. Any help would be great. Thanks. E.

Good you’re doing your research. You’re right, the FCRA affords you many consumer rights.

Answering your question, quoting the FCRA, if the Verizon account isn’t 100% accurate, complete, and verifiable, Equifax is reporting “erroneous” data that should be deleted from your credit file. You should dispute this by calling in or mailing a dispute to Equifax.

A dispute will open a case requiring Equifax to do a re investigation with the credit furnisher (Verizon). If the disputed data cannot be verified, is incorrect, or Equifax fails to complete the investigation within 30 days of your dispute, they are legally compelled to permanently delete the data from your credit file.

You also stated that the Verizon account is very old. If the date of non-payment on the account was over 7 years old, Equifax has no business reporting the derogatory. After 7-years, the collection account should have been deleted from your credit report. You can advise Equifax of this fact because they are illegally reporting negative data past the 7-year limit.

Note: Derogatory information remains on your credit report for 7 years, bankruptcy for up to 10 years, and positive information remains indefinitely.

Good Luck.

I seriously don’t think people really get what credit scores are, even though we hear about them all the time on tv! I still have one of the songs from FreeCreditReport.com’s tv ad’s jingle, but having a fun song stuck in my head does nothing to teach me about credit scores. I find it to be really cool that you have put together these 7 misconceptions about credit reports, because they are often not spoken about too much between credit companies and people who use credit cards. That point brings me to the real focus of my comment, do the terms of service (for say a credit card) tend to include information on credit reporting? It’s been so long since I enrolled for a credit card, as I’ve been using the same one for the past several years. It would be interesting to see where people are expected to get this information (aside from on the internet).

George, thank God for the Internet and sources like Wikipedia because whether willfully or legally, ZERO information is given to the public via credit card agreements. The same applies to the purveyors of credit data, the credit bureaus, which purposely intend to keep people in the dark about the true mechanics of credit scoring. But, aside from the web – and run while you can these brick and mortar bookstores are open – you can read some great credit repair and credit score literature in the likes of Barnes & Noble.

Really interesting to think about the books at Barnes and Noble on this topic. Honestly, I recall seeing a money/finance section there; but I typically view those books as sort of “scammy” in some way. Financial books and self-help psychology books both come across in the same way to me, and maybe I am right to a good degree; but I am realizing that there actually may be some good content in those books.

Oh, and I agree fully with you on the importance of websites like Wikipedia. I am actually starting to wonder if the recent SOPA/PIPA bills that were working their ways through the House of Representatives (in the USA) had anything to do with credit card companies or banks wanting to minimize access to information like this. Maybe that is just my conspiracy theory or something, but it doesn’t seem to far fetched to me!

A Conspiracy theorist, eh? Well, you’re certainly hitting the nail in the head about “BIG CORPORATIONS.” Oftentimes, society condemns BIG GOVERNMENT but we easily forget to keep a constitutional system of Checks and Balances on BIG CORPORATIONS, which are the driving force influencing the absurdity of lawmakers and bills like SOPA/PIPA.

Hopefully you are wrong about your theory because if passed, SOPA/IPA would have a crippling effect on our economy. Not only would SOPA/PIPA impact the likes of Facebook and Youtube, but it would lambaste government, inundating courts at a local, state, and federal level, and finally, it would impoverish banks, which would be the likely insurers of many plaintiffs that would be defending against SOPA/PIPA lawsuits.

You can definitely say that banks have a lot to do with the present state of credit bureaus, unfair credit reporting, and the consumer credit score.

Great post! I am so happy to learn that making too many hard inquiries within a proximate timeframe can hurt your future opportunities to obtain loans. I previously thought that ALL credit checks could hurt future credit and loan approvals.

Another misconception is that Every inquiry for credit costs 5 points. The fact is that there is no fixed set number of points that an inquiry will cost. Generally speaking, inquires have a relatively minor contribution to the overall score.

Hey these are some great points! A credit score will often consider the number of accounts or credit cards you carry that have a balance, in addition to your overall utilization of available credit. Thus, you may lose points for having a higher number of accounts with balances!

very nice post, i certainly love this website, keep on it

You know not a lot of people know about these 7 misconceptions about credit reporting and everything, Even I didn`t know half of them. Just like for example this one, “All credit inquiries hurt your credit score”. I could honestly say that I didn`t know that but now that I do I am going to need to be more careful with my credit!